Semiconductor Stocks Snap Back as the Fed is Split Down the Middle

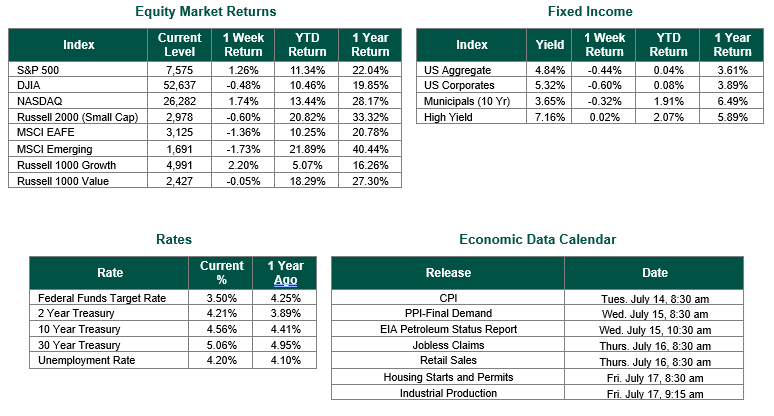

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 7575, representing an increase of 1.26%, while the Russell Midcap Index moved -0.33% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -0.60% over the week. Additionally, developed international equity performance and emerging markets were negative, at -1.36% and -1.73%, respectively. Finally, the 10-year U.S. Treasury yield closed the week at 4.56%.

Leadership swung back to the largest technology stocks last week, a sharp reversal from the prior week’s broadening rally away from the technology sector. Semiconductors, which stumbled into the third quarter with an 11.6% decline over the first two trading days of the month, snapped back to finish the week higher, with the iShares Semiconductor ETF (Ticker: SOXX) gaining 2.7%. Nvidia (Ticker: NVDA) rose roughly 4%, and Meta Platforms (Ticker: META) surged nearly 15%, its best respective week since early 2024, helping the technology-laden Nasdaq Composite lead the major benchmarks with a gain of 1.74%. Beneath the surface, however, breadth narrowed considerably. Eight of the eleven S&P 500 sectors declined on the week, with only the technology and energy sectors posting meaningful gains, and the Dow Jones Industrial Average gave back a portion of the prior week’s record run, falling 0.50%. Energy’s 3.1% advance came courtesy of geopolitics, as renewed hostilities between the U.S. and Iran, including strikes around the Strait of Hormuz and the apparent end of the ceasefire, drove West Texas Intermediate crude oil up more than 4% to the low $70s per barrel.

The week’s most notable single event came on Friday, when South Korean memory chipmaker SK Hynix began trading on the Nasdaq through an American Depositary Receipt (ADR) listing that raised $26.5 billion, one of the largest such offerings on record. Priced at $149, the shares opened at $170. They finished their first session of trading up roughly 14%, a strong signal that investor appetite for the artificial intelligence (AI) infrastructure trade remains intact despite the group’s early-quarter wobble. The debut was a fitting bookend to a week in which the AI complex reasserted itself, and it carried a measure of irony, as a selloff in South Korean semiconductor names helped spark the prior week’s global chip weakness.

On the policy front, Wednesday’s release of the minutes from the June 16-17 FOMC meeting, Chairman Kevin Warsh’s first at the helm, confirmed just how divided the committee has become. While the vote to hold the federal funds target range steady at 3.50% to 3.75% was unanimous, the minutes revealed that a few officials saw a case for hiking rates as soon as June. The accompanying projections showed that nine participants penciled in at least one hike by year-end, while eight expected no change and one expected a cut. Notably, Chairman Warsh declined to submit a rate projection of his own, becoming the first Fed chair to abstain since the “Dot Plot” chart was introduced in 2012. The move is consistent with his stated preference that markets take their cues from incoming data rather than from the Federal Reserve. Treasury yields drifted higher on the week, with the 10-year yield rising roughly nine basis points (i.e., 0.09%) to 4.56%, its highest level since late May.

Looking to the week ahead, Tuesday shapes up as maybe the most consequential day of the summer thus far. The June Consumer Price Index (CPI) will be released before the open. The second-quarter earnings season kicks off in earnest, with JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs, and Wells Fargo all reporting Tuesday morning. Chairman Warsh is scheduled to testify before the House Financial Services Committee later that morning. The June Producer Price Index (PPI) follows on Wednesday, with retail sales, weekly jobless claims, and the Philadelphia Fed manufacturing survey rounding out the calendar on Thursday. With the Fed emphasizing data dependence and its next meeting set for late July, this stretch of inflation and consumer data will go a long way toward shaping rate expectations. Consensus calls for another strong quarter of corporate profit growth, with forward guidance and margin commentary likely to matter as much as the headline numbers.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 7/10/26. Unemployment data sourced from the Bureau of Labor Statistics on 7/10/26. Weekly Jobless Claims are sourced from the U.S. Department of Labor. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Please note: Hennion & Walsh Asset Management currently may have allocations within its managed money program, and Hennion & Walsh currently may have allocations within certain SmartTrust® Unit Investment Trusts (UITs) consistent with several of the securities listed and themes described in this update.