Markets Climb on Peace Deal Hopes as SpaceX Makes IPO History

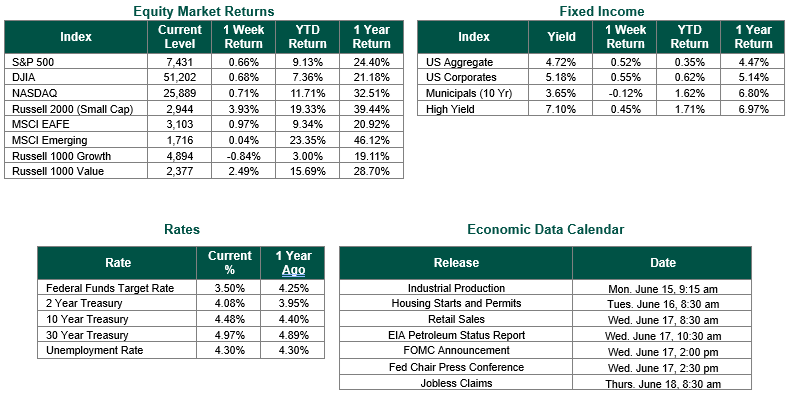

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 7431, representing an increase of 0.66%, while the Russell Midcap Index moved +2.30% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +3.93% over the week. As developed international equity performance and emerging markets were negative, returning +0.97% and +0.04%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.48%.

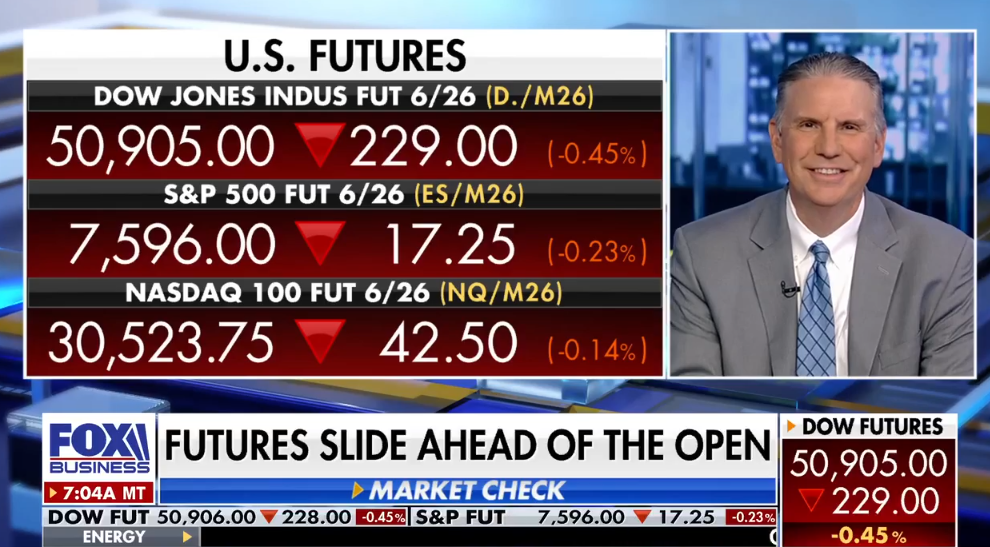

Last week was defined by historic developments on multiple fronts, a landmark initial public offering (IPO) that became the largest in history, intensifying optimism around a potential resolution to the U.S.-Iran conflict, and continued anticipation around the Federal Reserve’s first policy meeting under new Chairman Kevin Warsh. Overall, equities closed broadly higher for the week, brushing off a strong jobs report and modestly higher U.S. Treasury yields, as falling oil prices and easing geopolitical risk overshadowed lingering concerns about inflation and the future path of monetary policy. Crude oil fell roughly 7% on the week, pulling back to the mid-$80s per barrel as expectations for the reopening of the Strait of Hormuz pressured energy markets.

The most notable corporate event of the week, and arguably of the year, however, was the long-anticipated public debut of SpaceX. Priced at $135 per share on Thursday evening, the offering raised approximately $75 billion through the sale of more than 555 million shares, surpassing Saudi Aramco’s 2019 listing as the largest IPO in history. Shares opened at $150 on Friday morning and closed at $160.95, a gain of more than 19% from the IPO price, valuing the company at more than $2.1 trillion and instantly making it one of the largest publicly traded companies in the world. The deal featured an unusually large retail allocation of roughly 30%, far exceeding the typical 5-10% range, yet trading remained orderly despite enormous volume. While the bull case rests on SpaceX’s dominant position in launch services, the rapid scaling of Starlink, and investment opportunities within the aerospace & defense industry – notably in space-based data infrastructure, the valuation does demand significant scrutiny given last year’s reported operating loss of $4.2 billion on roughly $18.7 billion in revenue. Regardless of which side of the debate one falls on, the offering’s success is a notable signal for an IPO market that has been waiting for a true marquee deal and will likely lead to more IPOs down the road this year.

On the geopolitical front, the week culminated in a major breakthrough as the U.S. and Iran announced over the weekend that a peace agreement had been reached, with an official signing ceremony scheduled for Friday, June 19, in Switzerland. The framework agreement, mediated in large part by Pakistan and Qatar, calls for the immediate reopening of the Strait of Hormuz, the lifting of the U.S. naval blockade, an initial 60-day ceasefire, and the eventual easing of certain sanctions in exchange for Iranian concessions on its nuclear program. The Strait of Hormuz, through which roughly 20% of global oil shipments typically pass, has been largely closed since the conflict began on February 28, contributing to elevated energy prices and persistent stagflation concerns throughout the spring. The reopening should provide meaningful relief on the inflation front, easing pressure on both consumers and the Federal Reserve. However, investors will be watching closely for any signs of fragility in the agreement, particularly given Israel’s stated reservations and recent strikes in Lebanon. If the deal holds, the implications are significant: lower oil prices, easing headline inflation, improved global growth prospects, and a potentially more accommodative monetary policy path in the second half of the year.

The week ahead will be one of the most consequential of the year for monetary policy, with the June 16-17 FOMC meeting marking Chairman Kevin Warsh’s first as the head of the Federal Reserve. Warsh has publicly favored lower rates, but inherits a divided committee that currently has futures markets pricing in no rate cuts at this meeting and only modest easing through year-end. The focus will be less on the policy decision itself and more on the Fed’s updated Dot Plot chart and how Warsh communicates the path forward in his first post-meeting press conference, particularly given the recent shift in the inflation backdrop following the announced peace deal. May retail sales, industrial production, housing starts, and pending home sales will also be released this week. As a reminder, U.S. markets will be closed on Friday for the Juneteenth holiday.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 6/12/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.