Is There a New Sheriff in Town at the Fed?

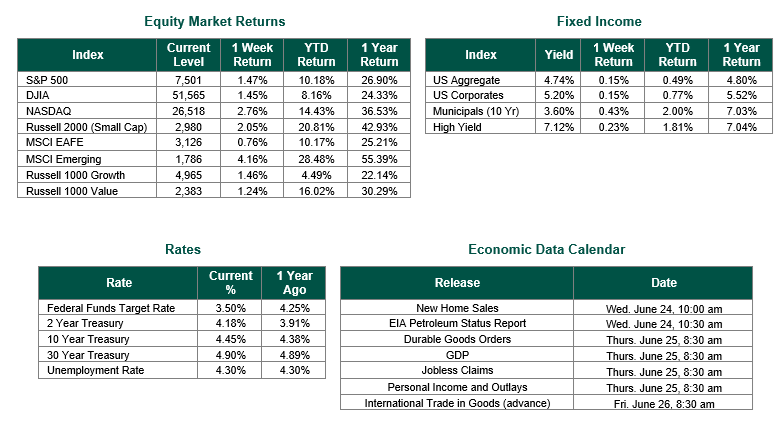

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 7,501, representing an increase of 1.47%, while the Russell Midcap Index moved +1.01% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +2.05% over the week. Developed international equity and emerging markets were also higher, returning +0.76% and +4.16%, respectively. Finally, the 10-year U.S. Treasury yield was little changed, ending the week at 4.45%.

The marquee event last week was the June 16–17 meeting of the Federal Open Market Committee (FOMC), the first chaired by Kevin Warsh. As widely expected, the Committee stayed “on pause,” voting unanimously to hold the Federal Funds Target Rate steady within a range of 3.50% to 3.75%. The decision itself was not the story; the projections that accompanied it were. With inflation sitting at a three-year high and a war-driven energy shock still working through the economy, the statement described an economy “expanding at a solid pace” and inflation that “remains elevated relative to the Committee’s 2 percent goal,” while removing the language that had previously signaled a bias toward future rate cuts. The post-meeting statement was dramatically shortened to roughly 130 words, less than half the length of the prior release, an early signal of the more streamlined communication style the new Chair has long advocated.

The larger shift from the FOMC came in the projections that accompanied the decision. Back in March, the Committee had penciled in one 25-basis-point rate cut in 2026 and another in 2027. The updated Dot Plot told a very different story: the Fed now forecasts approximately one 25-basis-point rate hike in 2026, followed by approximately one 25-basis-point cut in 2027. That said, the path among the eighteen voting members who provided projections is far from settled: nine forecast a single rate hike this year, eight forecast no change, and one still anticipates a cut. The accompanying Summary of Economic Projections reinforced the more cautious inflation outlook: the Committee revised its 2026 real GDP growth projection to 2.2% (from 2.4% in March), lowered its year-end 2026 unemployment forecast to 4.3% (from 4.4% in March), and raised its core PCE inflation forecast, the Fed’s preferred inflation gauge, to 3.3% for 2026 (from 2.7% in March), before easing to 2.5% in 2027 and back toward its 2% target in 2028. In a notable break from precedent, Chair Warsh declined to submit his own “dot,” encouraging his colleagues to continue offering projections while refraining from doing so himself, consistent with his long-held view that the practice “is not helpful in the conduct of policy.”

Beyond the numbers, Chair Warsh used his first press conference to make clear that meaningful change is coming to the Fed, signaling his intent to reshape how the central bank operates, communicates, and pursues its dual mandate through a series of task forces, albeit in no immediate rush, with the goal of more accurate data, less conflicting rhetoric from individual governors, and a more durable form of “price stability,” a phrase he returned to repeatedly. While some analysts now look for a hike as early as October and others expect no change at all in 2026, we lean toward the latter for the immediate future, contingent on the U.S. and Iran agreement holding, the Strait of Hormuz reopening on a sustainable basis, and oil prices and their inflationary pressures continuing to recede.

Markets did not take the hawkish turn in stride at first. Equities sold off sharply on Wednesday following the announcement, with the S&P 500 posting its weakest “Fed Day” under a new Chair since 1994, before recovering much of that ground on Thursday. U.S. markets were then closed on Friday for the Juneteenth holiday. The rebound on Thursday, combined with notable strength in emerging markets, left the major indices higher on the week.

This week’s data calendar will test the Committee’s hardened stance: releases include Thursday’s Personal Income and Outlays report, which contains the PCE price index, alongside the third estimate of first quarter GDP, Durable Goods Orders, and jobless claims on Thursday, New Home Sales on Wednesday, and the advance International Trade in Goods report on Friday. With equities near record highs, the market has set a high bar for the incoming inflation data to clear, leaving short-term bouts of volatility unsurprising.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 6/18/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but it does not ensure a profit or guarantee against a loss.