Yields Surge Amid Hawkish Fed Signals

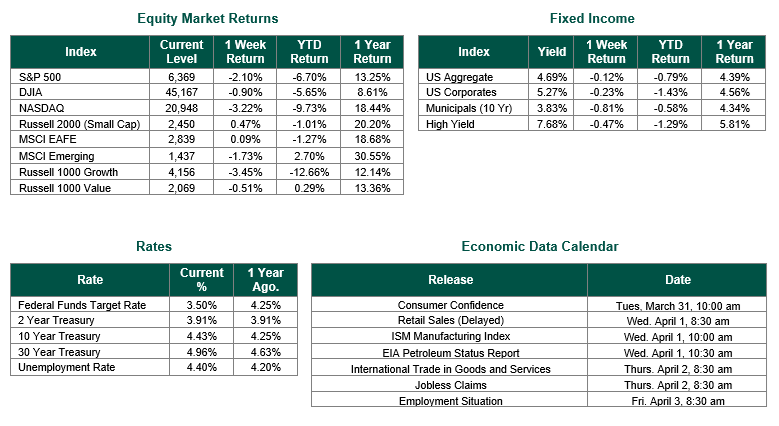

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 6369, representing a decrease of 2.10%, while the Russell Midcap Index moved -1.64% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned +0.47% over the week. As developed international equity performance and emerging markets were mixed, returning 0.09% and -1.73%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.43%.

Last week, key US economic data releases included flash S&P Global Purchasing Managers’ Index (PMI) on Tuesday, with the composite PMI at 51.4, signaling modest expansion but slightly below the prior 51.9. Initial jobless claims for the week ending March 21, reported on Thursday at 210,000, up 5,000 from the previous week, yet with a stable 4-week moving average of 210,500. On Friday, the University of Michigan consumer sentiment index fell to 53.3 amid surging gas prices and Middle East tensions, from 56.6 in February.

The rise in U.S. Treasury yields over the past week appears to stem from a mix of elevated inflation concerns, tighter-than-expected Federal Reserve signaling, and ongoing geopolitical and oil-price uncertainty linked to the Iran-related conflict in the Middle East. Markets have dialed back expectations for near-term Fed rate cuts as recent data, including strong inflation and a hawkish‑leaning tone at the latest meeting, have led investors to price in a less accommodative policy path, which lifts short‑ and medium-term yields. At the same time, elevated oil prices and heightened geopolitical risk have pushed up risk‑adjusted discount rates across the curve, while resilient growth and elevated Treasury supply have reinforced the perception that longer‑term real yields and term premiums need to stay higher to compensate investors for inflation, duration, and fiscal‑risk exposure.

Federal Reserve governors delivered several addresses focusing on future monetary policy.

Federal Reserve Governor Stephen Miran said he has raised his projection for the federal funds rate at year‑end by about half a percentage point, arguing that recent upside surprises in inflation—not geopolitical developments or oil prices—justify a somewhat less accommodative path and put his preferred policy rate closer to a neutral setting that neither stimulates nor restrains growth. He stressed that, while it is too early to draw firm conclusions about how higher oil prices tied to the Iran conflict will pass through to broader inflation, monetary policy should avoid either “slamming on the gas” or holding the economy back unnecessarily in the face of such shocks.

In his address, Richmond Fed President Thomas Barkin described a deepening “economic fog” caused by the escalating war with Iran and the rapid integration of artificial intelligence. He noted that while inflation progress had already appeared to stall in recent months, the conflict’s resulting oil price shock and supply chain disruptions have introduced significant new risks to the outlook. Barkin characterized the current labor market as “fragile,” citing near-zero job growth despite low unemployment, and expressed concern that rising gasoline prices could further unsettle consumer sentiment and spending. Given these uncertainties, he maintained that it was “prudent” for the Federal Reserve to hold interest rates steady at the higher end of the neutral range while awaiting more clarity on the economy’s direction.

Our view is that trying to play the Fed guessing game is often counterproductive and an exercise in futility. However, with the Fed’s stated neutral rate at 3% (just 50 Bp lower than the lower bound of the Federal Funds Target Rate range today), investors should not expect too much from the Fed this year in terms of interest rate cuts, unless, of course, there is a serious deterioration in the labor market or inflation comes down considerably.

Our thoughts and prayers continue to be focused on the brave Men and Women of the U.S. Military and our Allies during this conflict in the Middle East.

Equity and Fixed Income Index returns sourced from Bloomberg on 3/27/26. PMI data are sourced from S&P Global. Weekly Jobless Claims are sourced from the U.S. Department of Labor. Consumer Sentiment data are sourced from the University of Michigan. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.