A Rocky Week For U.S. Markets & Economy

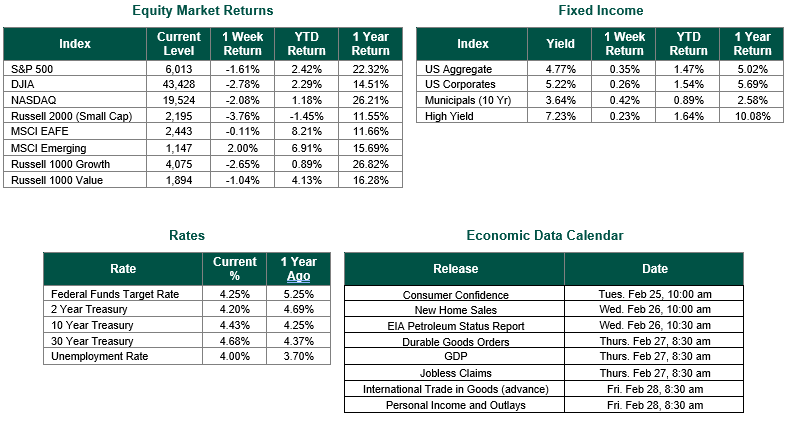

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 6,013, representing a decrease of 1.61%, while the Russell Midcap Index also moved lower by over 2.50% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -3.76% over the week. As developed international equity performance and emerging markets were mixed, returning -0.11% and 2.00%, respectively. Finally, the 10-year U.S. Treasury yield moved slightly lower, closing the week at 4.43%.

Last week was a turbulent one for the U.S. stock market and economy, marked by sharp declines, economic unease, and policy uncertainty. As mentioned above, the major indexes took a hit, with the Dow Jones Industrial Average dropping 2.5%, its worst weekly performance since October 2024. This downturn erased earlier gains in the holiday-shortened week, leaving all three major U.S indexes in negative territory for February so far.

A mix of disappointing economic data and corporate developments triggered the sell-off. UnitedHealth Group’s shares plunged over 7% after reports surfaced of a Department of Justice (DOJ) investigation into its Medicare billing practices, dragging the Dow Jones Industrial Average lower. Meanwhile, consumer spending fears intensified after Walmart issued a weaker-than-expected outlook, signaling potential cracks in consumer demand. Existing home sales also came in below forecasts, hampered by high mortgage rates and prices, while consumer confidence weakened amid rising inflation expectations and tariff uncertainties.

Tech stocks, a key market driver, weren’t spared either. Nvidia, a darling of the artificial intelligence (AI) boom, dropped 4.1% ahead of its earnings report, contributing to a 2.9% decline in the “Magnificent Seven” group of mega-cap stocks. In addition, cloud services provider Akamai Technologies saw a dramatic 21.7% fall after a disappointing 2025 revenue outlook, underscoring broader concerns about near-term growth in the sector.

Economic indicators painted a mixed picture last week. The S&P Global U.S. Services PMI slipped into contraction territory at 49.7, the first such reading in 25 months, hinting at a slowing service sector. Conversely, manufacturing PMI edged up to 51.6, an 11-month high, offering a sliver of optimism. However, the overarching narrative was one of caution, fueled by President Trump’s tariff threats on lumber, cars, and pharmaceuticals, which added volatility and stoked potential inflation fears.

During the week, investors shifted toward defensive assets like consumer staples, with names like Procter & Gamble and Kraft Heinz gaining ground. Gold hovered near $2,950 an ounce after hitting a record high, while oil prices dipped 3% to $70.25 per barrel. As the week closed, Wall Street braced for more uncertainty, with tariffs, consumer sentiment, and upcoming earnings in focus. For now, the collective mood of investors appears to be cautious, reflecting an economy at a crossroads and a bull market that is over two years old.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 2/21/25. Earnings data sourced from FactSet on 2/21/25. PMI sourced from S&P Global on 2/21/25. Economic Calendar Data from Econoday as of 2/24/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.