A Week of Resilience

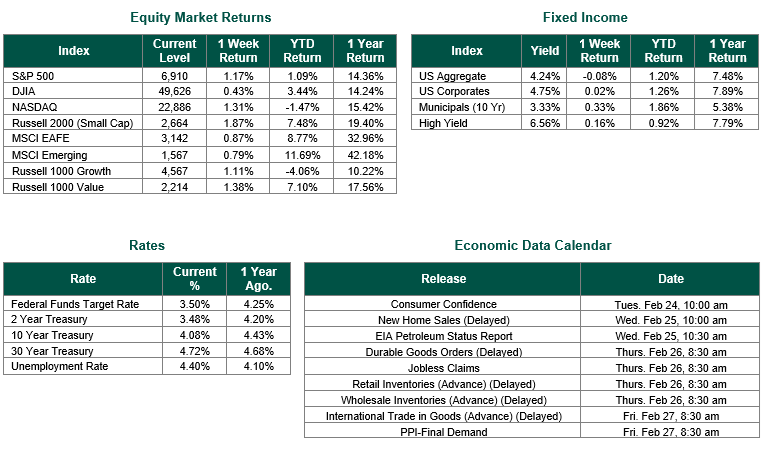

Global equity markets finished positive for the week. In the U.S., the S&P 500 Index closed the week at a level of 6910, representing an increase of 1.17%, while the Russell Midcap Index moved +1.08% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 1.87% over the week. As developed international equity performance and emerging markets were positive, returning 0.87% and 0.79%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.08%.

Stocks found their footing last week after a rough recent stretch, with the S&P 500 rising roughly 1.1% and reclaiming a key technical level, its 50-day moving average. Technology stocks led the recovery, particularly in semiconductors and artificial intelligence (AI) hardware. At the same time, software companies continued to lag as investors questioned whether traditional software businesses could hold their ground in an AI-driven landscape. Cyclical and consumer-facing sectors also contributed to the week’s gains, with a handful of solid earnings reports reinforcing that the broader corporate earnings picture remains intact.

The headline economic story was Friday’s Q4 2025 gross domestic product (GDP) report, which came in at just 1.4% annualized growth, well below the 2.5% consensus estimate. The miss, however, was largely driven by a sharp pullback in federal government spending tied to November’s government shutdown, a one-time drag that most economists expect to reverse. Consumer spending remained healthy at 2.4% growth, and underlying private demand held firm. On the inflation front, December personal consumption expenditures (PCE) data showed prices ticking back up month over month, keeping the Fed’s path forward for interest rates uncertain.

The Federal Reserve’s latest meeting minutes confirmed a cautious, divided committee and one that sees no urgency to cut rates and isn’t ruling out a hike if inflation proves stubborn. The Supreme Court’s ruling striking down broad tariffs under IEEPA added a jolt of headline volatility midweek, though markets absorbed it relatively well. The Trump administration quickly signaled plans to pursue alternative trade authority, keeping the tariff story alive heading into the new week.

This week brings Nvidia earnings on Wednesday which will provide a critical read on the AI investment thesis, along with more inflation data and several major retail earnings reports. With markets having shown resilience in the face of disappointing GDP and tariff noise, the near-term question is whether stabilization can translate into sustained momentum.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 2/20/26. GDP sourced from the Bureau of Economic Analysis. PCE data from the BEA on 2/20/26. FOMC minutes from the Federal Reserve on 2/18/26. Calendar Data from Econoday as of 2/23/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but does not ensure a profit or guarantee against a loss.